Setting goals for you and your business in 2024

The new year is a new beginning. If you are a business owner, this is often the time of year when you reflect on where you are at and think about your business goals for the year ahead.

Setting goals is an essential part of personal and professional growth. These could be lofty goals, or even setting out a plan to achieve some more mundane (but equally important) projects. Whether that is getting paid faster, reassessing expenses or bigger things like automation of processes and new markets. You may be looking to expand your business or create more time for yourself.

Having a clear vision and actionable goals can help you achieve your long-term plans. Here are some tips to get you started:

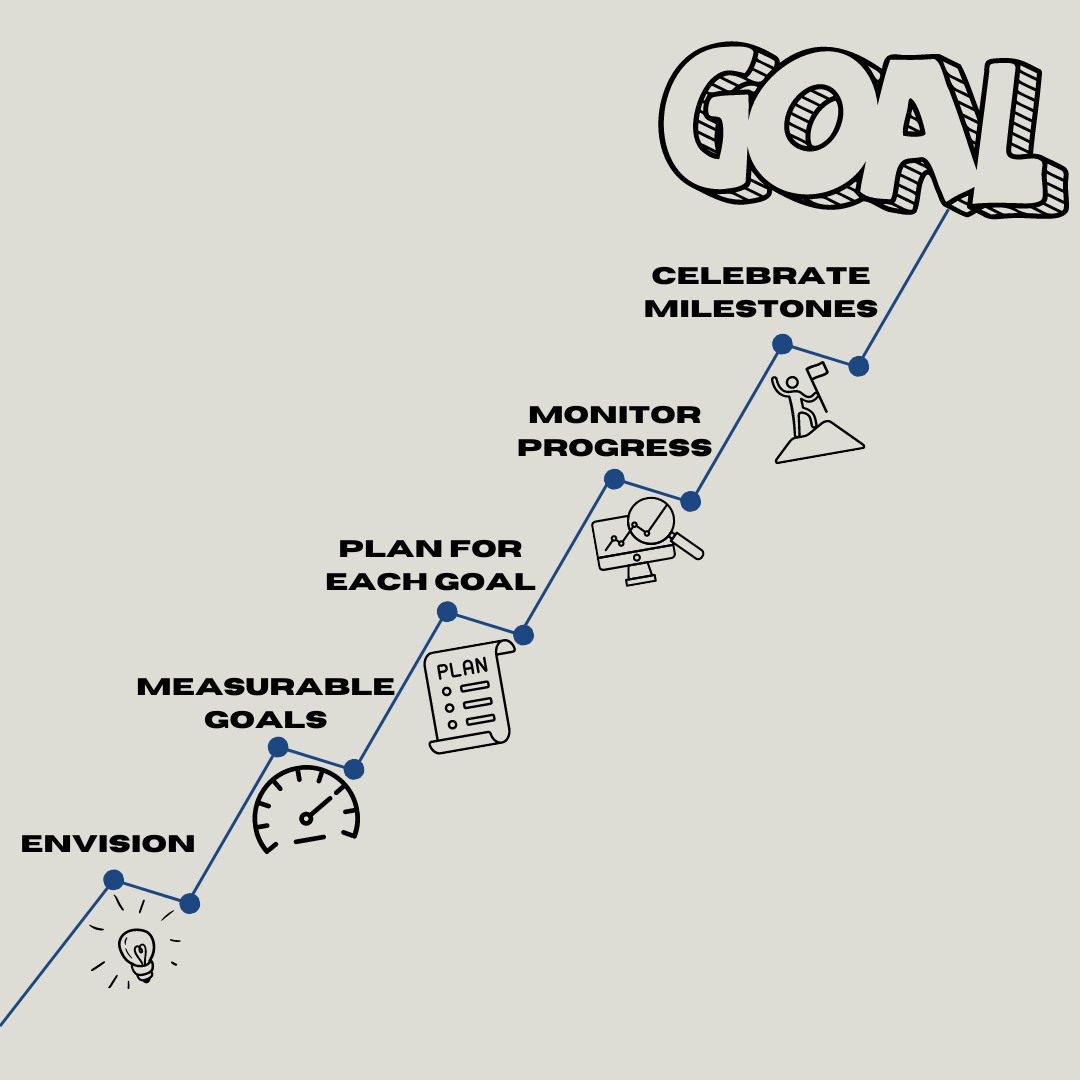

- Envision your future:

Reflect on what you truly want from your life and how your business can help you achieve those aspirations. Consider where you want your business to be in the next five or ten years. Having a clear endpoint in mind will make it easier to set goals that align with your vision.

- Set measurable goals: Vague goals can be challenging to track and evaluate. Instead, focus on setting goals that are measurable. Think about the key metrics you already monitor in your business and how you would like to see them improve. For example, aim for a 3% increase in net profit year-on-year, a 2% reduction in expenses, or acquiring two new customers per month or grow your prospect database by 50%. If you set specific targets, you can easily track your progress and make adjustments as needed.

- Develop a plan for each goal: Once you have identified your goals, it's crucial to create a plan of action to achieve them. This can be as simple as jotting down your ideas or engaging in a brainstorming session with your team or advisors. Having a well-defined plan in place will help you stay focused and motivated to follow through.

- Monitor your progress regularly: It's essential to regularly check in on your progress towards your goals. Set reminders on your calendar or align your monitoring process with your invoicing cycle. By consistently evaluating your progress, you can identify any areas that need improvement or come up with fresh ideas to help you reach your targets.

- Celebrate your achievements: Celebrating milestones along the way is crucial for maintaining motivation and momentum. Plan a reward for yourself when you achieve a significant goal. It could be treating the team to a morning tea, having a day out of the office together or planning an event for the end of the year. Choose something that brings you joy without breaking the bank.

Not sure how to get started?

We can help you with the strategy and identifying the information you’ll need to track, so you can monitor your progress.

Setting goals is just the first step. By implementing these tips and staying committed to your vision, you can turn your long-term plans into reality.