Reserve Bank of Australia Update - March 2024

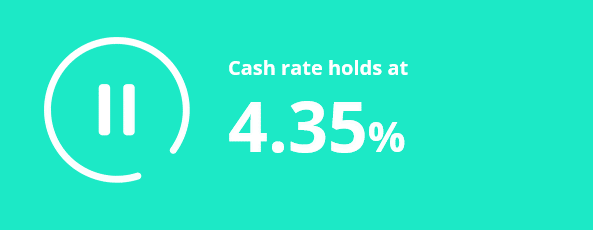

The March Board meeting of the Reserve Bank of Australia (RBA) concluded with a decision to maintain the official cash rate at 4.35%, following a thorough review of recent economic indicators. The official statement for this decision is available on the RBA's website.

This decision is in line with what was anticipated by the market, providing stability for borrowers in Australia who have variable interest rate loans, especially in light of recent rapid rate increases.

Although inflation has exceeded the target range of 2% to 3%, registering a 3.4% rise in the twelve months leading to January, the RBA's decision to maintain the rate allows for a continued assessment of the effects of previous rate adjustments.

The RBA board remains committed to bringing inflation back within the target range. Recent data indicates a moderation in inflation, with the headline monthly CPI holding steady at 3.4% over the year to January, showing a gradual decline in momentum driven by a decrease in goods inflation. Despite this, services inflation remains high but is slowing at a more gradual pace. These trends reflect ongoing excess demand in the economy and robust domestic cost pressures, both in labour and non-labour inputs.

The board emphasised the importance of ensuring that inflation is on a sustainable path towards the target range, noting that medium-term inflation expectations have thus far been consistent with the target, and it is crucial to maintain this alignment.

Property Market Snapshot

When was the last time you looked at your SMSF loan interest rate?

In today's rapidly changing financial landscape, it's essential to stay ahead of the curve when it comes to maximising your financial opportunities. That's why we're excited to bring you valuable insights into Self-Managed Super Fund (SMSF) borrowing and refinancing, two strategies that could significantly impact your financial future.

SMSF loans are often an untapped resource, offering unique advantages for property investment within the framework of your superannuation. With competitive rates and a growing number of lenders entering the market, now is the perfect time to reassess your SMSF borrowing arrangements.

Refinancing your SMSF loan or conducting a health check on your current setup can potentially unlock large savings and ensure your borrowing strategy remains aligned with your goals. We’re here to guide you through this process, leveraging our expertise to help secure the favourable terms and rates tailored to your needs.

Here are some key tips to consider when exploring SMSF lending:

Evaluate Your Current Loan: Take the time to review the terms, interest rates, and fees associated with your existing SMSF loan. Refinancing could potentially lead to significant cost savings or improved features.

Understand Lender Requirements: Different lenders may have varying criteria for SMSF loans. Make sure you understand their requirements regarding property types, loan-to-value ratios, and repayment structures.

Seek Expert Advice: SMSF borrowing involves complex legal and financial considerations. Consult with professionals who specialise in SMSF lending, such as mortgage brokers, accountants, and financial advisors, to ensure compliance and optimal outcomes.

Assess Investment Opportunities: Conduct thorough due diligence on potential property investments within your SMSF. Consider factors like location, rental yield, and potential capital growth to make informed decisions.

Regularly Review Your Strategy: Market conditions and personal circumstances can change over time. Regularly review your SMSF borrowing strategy to ensure it continues to meet your objectives.

By partnering with the right mortgage broker, you can potentially gain access to a wealth of industry knowledge and a diverse range of lending options.

If you're considering SMSF borrowing or refinancing, we're here to help. Reach out to schedule a free consultation, and let's take proactive steps towards optimising your financial future.

How does the decision affect you?

The cash rate significantly shapes interest rates throughout the economy, impacting lending and deposit rates. Consequently, these interest rates play a crucial role in influencing economic activity, employment levels, and inflation rates.

This broad influence has widespread implications for many individuals in Australia.

If you would like to discuss what today’s news means for you and your finances, please feel free to contact us to arrange a discussion in more detail.